Overview

![]() The Continental Finance Verve card is a credit card marketed to applicants who have “less-than-perfect credit.” It is an unsecured credit card, meaning that it does not require a deposit before supplying the cardholder with a line of credit. However, the company may require an applicant to pay a security deposit if the applicant does not qualify for the unsecured version of the card. The Verve card comes with a $500 credit limit (subject to variation depending on creditworthiness) and does not offer an attached rewards or cash back program.

The Continental Finance Verve card is a credit card marketed to applicants who have “less-than-perfect credit.” It is an unsecured credit card, meaning that it does not require a deposit before supplying the cardholder with a line of credit. However, the company may require an applicant to pay a security deposit if the applicant does not qualify for the unsecured version of the card. The Verve card comes with a $500 credit limit (subject to variation depending on creditworthiness) and does not offer an attached rewards or cash back program.

Continental Finance used to offer two credit cards called the Matrix card and the Cerulean card in partnership with Discover, but the company is now a MasterCard partner and only advertises the Verve card on its homepage. The Continental Finance website still includes a login page for Matrix and Cerulean users, but it is unclear whether the company is still issuing copies of these cards.

On February 4, 2015, Continental Finance was ordered by the Consumer Financial Protection Bureau to refund $2.7 million in illegal credit card fees to cardholders and. The CFPB issued a statement announcing this order, a portion of which is excerpted below:

Today, the Consumer Financial Protection Bureau (CFPB) ordered Continental Finance Company LLC, a subprime credit card company based in Delaware, to refund an estimated $2.7 million to approximately 98,000 consumers who were charged illegal credit card fees. The agency found that the company’s “fee-harvester” subprime credit cards misrepresented certain fees and hit consumers with illegal charges. The order also requires the company to pay a civil penalty of $250,000.

“Continental Finance misled consumers and charged them illegal fees,” said CFPB Director Richard Cordray. “These excessive fees are especially harmful because the cards were targeted to consumers with subprime credit who are often economically vulnerable. We will act to protect people who are wronged in this market.”

The CFPB’s full order can be seen here.

Continental Finance Verve Card Fee Breakdown

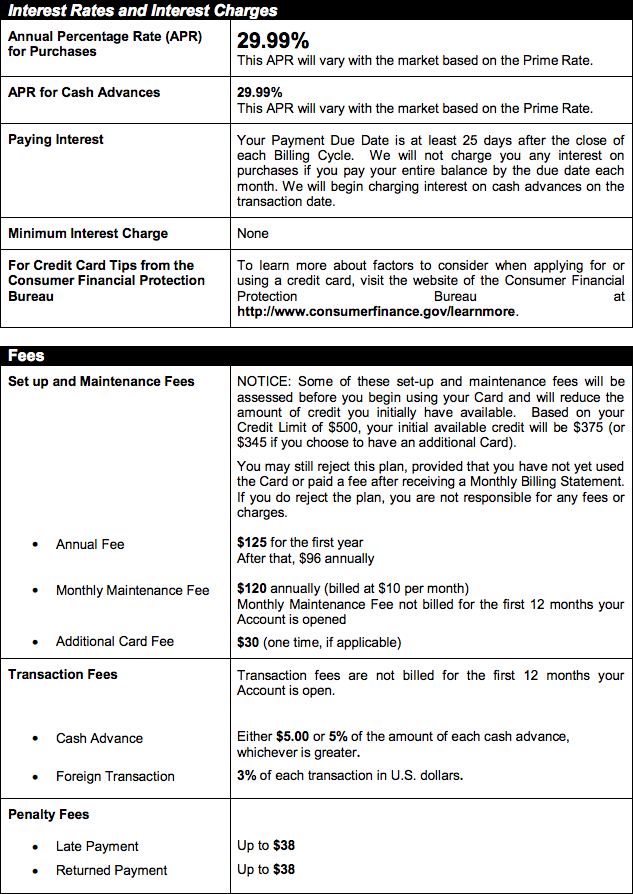

The Verve card charges an annual fee of $125 for the first year of service ($96 for each subsequent year), a $10 monthly fee beginning in the second year, a $30 additional card fee (if applicable), a cash advance fee of $5 or more, a foreign transaction fee of 3%, a late payment fee of up to $38, a returned payment fee of up to $38, and an APR of 29.99% on carried balances. The card may also require a variable security deposit depending on the applicant’s creditworthiness, in which case it would function as a secured credit card. The default credit limit for a Verve card is $500, but users will only have access to an initial credit line of $375 after the first year’s annual fee has been applied.

Continental Finance Verve Credit Card Fees

At a glance

Founded: 2005

Location: Newark, Delaware

Issuer: Mid America Bank & Trust Company

Website: continentalfinance.net

Phone number: 1-866-449-4514

E-mail: n/a

What other reviewers are saying

Ripoff Report

![]() The Verve card only is only explicitly mentioned in three Ripoff Report complaints, but Continental Finance has received 84 complaints overall. The complaints that are specifically filed against Verve mention billing issues, excessive fees upon signup, and confusing payment schedules. The complaints leveled at Continental Finance overall echo those filed against Verve, but are often directed at other cards like the Matrix or Cerulean card. It is reasonable to assume that the service-related complaints against Continental Finance are also applicable to the Verve card, but specific pricing complaints are likely not relevant across the board.

The Verve card only is only explicitly mentioned in three Ripoff Report complaints, but Continental Finance has received 84 complaints overall. The complaints that are specifically filed against Verve mention billing issues, excessive fees upon signup, and confusing payment schedules. The complaints leveled at Continental Finance overall echo those filed against Verve, but are often directed at other cards like the Matrix or Cerulean card. It is reasonable to assume that the service-related complaints against Continental Finance are also applicable to the Verve card, but specific pricing complaints are likely not relevant across the board.

The Better Business Bureau

![]() Continental Finance has a “B” with the BBB and is not accredited at this time. The company has received 200 complaints in the last three years, with 101 of these related to billing and collection and 92 tied to product or service issues. The company has successfully resolved 199 of these complaints, while the remaining complaint was unresolvable due to an inability to contact the complainant. The company also has received two negative informal reviews and one positive informal review. The BBB cites the government action taken against the business as a major factor lowering its rating.

Continental Finance has a “B” with the BBB and is not accredited at this time. The company has received 200 complaints in the last three years, with 101 of these related to billing and collection and 92 tied to product or service issues. The company has successfully resolved 199 of these complaints, while the remaining complaint was unresolvable due to an inability to contact the complainant. The company also has received two negative informal reviews and one positive informal review. The BBB cites the government action taken against the business as a major factor lowering its rating.

Other sources

The Continental Finance Verve card has one negative user review on Credit Karma. This review was posted to a page of reviews for the Matrix card, and it awards Verve one out of five stars. Beverly Harzog’s credit card blog also gives the Verve card a negative review overall.

Featured User Reviews

I needed a credit card for an unexpected trip. The first thing they do is bill you $125 processing fee. Then they ask for a payment that day. (You can tell them you are paying on the due date). So I get my statement. My payment is due on the 27th of the month. So I pay my July payment on July 25th, I pay my August payment on August 27th and then I make my September payment on September 3rd. So now I am ready to make my October payment by October 27th. I get an email on October 7th, telling me that my payment is past due and now I owe 105.00. WHAT??? I call them and I am told that because I paid on the September payment on the 2nds, it was processed as an extra August payment and so therefore I am late. So now I still owe September and I owe October and a $35 dollar late fee. She said if I would have paid on September 4th it would have been the September payment. She would not help me but got a supervisor. I got the same runaround and he said he will talk to corporate. So now, although I paid my payment early, I owe late fees, an extra month payment and they are turning me over to credit bureaus as a late pay. I am cutting this card up and paying these loan sharks off ASAP. Don’t do business with them!!

-Dawnee, Ripoff Report

Just wanted to leave some comments for people who are considering obtaining this card.

I have had the card for about 7 months now. I received a preapproval offer in the mail in mid-2014, applied online, and received the card shortly thereafter. I called to activate, and the rep had me set up the first payment over the phone (toward the $125 annual fee), for which there was no additional fee.

I charge one or two things each month, then set up a payment on the card’s website to post by the due date. It takes several days after the payment posts for an equal amount of the credit line to become available again – unlike some card issuers, they’re being quite careful in covering themselves in case your payment bounces.

Otherwise, I’ve had no problems – no extra fees, no cases of the card being declined, no hassles. The card reports accurately to the credit bureaus each month.

If you’re trying to build or rebuild credit, this is not a bad way to go – this may be one of the few cards you can qualify for without a full security deposit, and as long as you pay on time each month, it will help your score. I recommend leaving a small balance ($20 or so) on the card at the close of each cycle to help with the utilization part of your score.

Once your score has improved enough to qualify for something better, you can close this card and escape the high annual fee.

I can’t say anything about credit line increases – I haven’t seen one yet, after 7 months of on-time payments, but I also haven’t asked for one.

-Keith Murray, Beverly Harzog’s Blog

Our take

Like the First Premier credit card, the Verve card is a less-than-ideal credit repair option for most applicants who have bad credit. It carries high annual and monthly fees and charges an APR that is much higher than industry averages. Cardholders on strict budgets could easily find themselves mired in fees if they miss even one payment with this card, and there are many better secured options out there with similarly low credit requirements.

There’s also the matter of the government action taken against Continental Finance. The fact that the company has incurred large punitive fines for inappropriately charging its customers is a major red flag that would make any card look bad. But when the card already looks bad on its own terms? Our opinion is that it is best to stay away from the Verve card completely.

Have you used a Verve credit card? Tell us about your experience in the comment section below:

This is the worst card I have ever had. I wish I would have never got the card. It was fine for the first 6 months or so. I had no issues, and understood all of my fees, etc involved with this card. Last month the problems started. I sent my payment via mail, as I always have. I sent it in 2 1/2 weeks before it was due. I kept checking my account to see if the payment posted. My payment did not post until a week and a half after it was due. By this time, I had received the bill for the next month. It was $92 after late fees. I was upset, but I assumed that the payment must have been lost in the mail or there was a mix up or something. So, I immediately sent the payment in, so I wouldn’t have the same issue again, just in case. This has been 3 weeks ago. My payment due date was yesterday, and I called to check and make sure that the payment had posted. Same issue. My payment has STILL not posted. All other payments have posted within a week. I am not going to pay online or over the phone to pay an additional $10.95 or whatever their fee is. I don’t pay my bills online, because maybe I am old fashioned and don’t prefer to do everything online for my own security. Plus, I don’t like auto payments in case my account needs to be used for an emergency, or something and I need my money. This card is a mistake. I will pay them one more time, but I am cutting this card up, paying it off if they can process the payment, and never using it again. If you have not got this card yet, I highly suggest that you reconsider or look into other options or you will be disappointed in the long run. Was also promised an increase after 3 or 6 months, and I never got one. Coincidentally the 6 month period is when they seemed to stop processing my payments on time.

This is the worst card ever, It’s a rip of card they need to close the bank immediately.

The card is designed for consumers trying to rebuild their credit and if you understand their requirements you should be alright. The card is really a credit card you start out with and after 6 months to a year of responsible usage, you upgrade to a better card.

How do I close this card? I just paid it off 7 days ago and the payment cleared my bank the next day. Still not available in my credit. Even though they payment has already cleared. It today’s banking industry, ACH payments are processed within 1 to 2 days. They are making people believe that their payment may be returned when paying online and that is the reason for the delay. That is simply not true for ACH payments. If they were processing a paper check, then I could see the delay of 4 or 5 days. I know all of this because I worked for a credit union for 25 years. They are simply taking advantage of people in unfortunate circumstances and should be held accountable. I will be closing out my account before my annual fee comes due so that I don’t pay these loan sharks another dime.

Please stop Continental Finance from facilitating fraud and theft of their customer’s banking information by:

1.) Failing to drug test employees, who with known substance issues, have ready access to banking information.

2.) Failing to do any criminal background checks. They employ known felons. Turnover, Supervision included, is 90%. Many people who quit seemed only interested in debit card information. It is quite common to have police arrest employees on the premises for various reasons, including stealing banking information.

3.) Criminal negligence in failing to enforce lip-service, useless office memo directives. It is common to have both Customer Representatives and Management access either cell-phones, writing instruments and scrap pieces of paper, or even an electronic notepad on company computers where banking information can be saved and retrieved later at one’s convenience. Each Customer Representative processes between 10-20 debit card payments daily. Much of the fraud happens during debit card payments where account numbers are put in the “joint name” space provided by Western Union’s “Speedpay” product portal. Western Union and MasterCard then become accessories in these criminal enterprises to defraud and steal from customers often poor, elderly, or criminally deceived by fraudulent claims and assurances.

4.) Despite fines for not sending statements, Continental Finance still does not provide regular delivery of statements. The company will refund only one late fee a year and seems not to process payments, in a timely fashion, so that customers incur late fees.

5.) The website is another scam. It does not allow all customers easy access at all times. Numerous complaints can be heard during phone calls of customer’s complaining about not being able to use the website. While company policy is to process such instances without the normal $10.95 fee, nothing is done in the way of late fees resulting in the web site not allowing access. Also, the website is not always clear about the inability to process debit or credit cards on the website (Continental Finance which charges a $125 annual fee for a $500 card, over 30% interest, and $37 late fees, still would like to charge their customers, a $10.95 fee to pay their bill.). Transactions will go thru, but are returned days later as “unrecognized” by the bank. The customer is given no notice. Late Fee incurs. Criminal. Like everything Continental Finance does, there is plausible deniability, or blaming poorly trained felons and drug users, in treating each customer as a mafia “mark”, then a valued partner in providing means and services.

PLEASE STOP CONTINENTAL FINANCE!

What a joke. I have had a very sick mom in the hospital and went online to make a payment like I always do. I put in my all the same info like I always had. The online payment tells me my info is incorrect and then locks me out of my account.. Huh.. What.?? My mom is out of hospital and doing ok so I take care of some business like this that I had to do. I call to see if I can make a payment and get my $25.00 late fee reversed… No I can’t because they already reversed a late fee for me back in last November .. How is this my fault that there computer system wasn’t working right and I was even told that by the representative… This is so sad…. Wow.. They can have the $25.00 dollars and I hope the CEO of this company can easily rest his head at night.. Because from the looks of all these reviews it seems he has got a real poop show going on… I thank them for helping me out during this very difficult time in me and my families life… Do your self a favor and don’t get a verve credit card…

I had this card for a year and it help me boost my credit score and the reps are friendly i had no trouble thanks verve for helping me to rebuild my credit score i pay my bill on time

I’m going to let you know that they are alive and well committing the worst possible atrocities against their customers( read:SUCKERS). Despite 2 class action lawsuits, they are still ripping off folks. WOW. I think it’s time for a third lawsuit, and I would be happy to join in such an endeavor.

Listen… The card is what it is….if you have bad credit and no options, then get the card. I did and I use it and then pay it off. High interest rates are to be expected when you have bad credit. They took a chance on me when no one else would not. I understood what I was getting into. I will use the card to rebuild and move one. Since opening in August 2015, I have an unsecured capital one $2k credit limit old navy $750 credit limit and a new car. Pay on time. They do hold your payment for 7 days before posting but just use this to rebuild and move on!!

This is the worst credit card ever. The biggest ripoff with all the charges. Its a let you know your low card. I wouldn’t suggest to my dog to get a card to buy his own food

I have had the card for close to a year now and have made on time payments of several hundred dollars each month. What type of credit increase can I expect on the anniversary?

Also, FYI, I’ve had no issues with the website and my on-line payments started being credited to my account on the next business day after about the first 6 months or so. The 8 days in the beginning was certainly not convenient, but not unexpected. Yes, paying $96 for a $500 line is borderline usury, but these are the choices we make when we don’t keep our financial houses in order.

I’ve had this card for a long time. It’s the worse thing I’ve ever done. On line payments are a constant problem. Security questions respond that the answer is incorrect. What, I don’t know my own info?? After calling the VERY RUDE rep, she said there’s a 10.95 fee !!! A supervisor posted it after an argument. Don’t do business here

I been having the same problem every single months

I have had this card for a year and a half now, yes the opening fees are high and they do charge a monthly maintenance fee, I had to pay only a 50.00 security deposit to open a 500 credit line. I have not received a CLI yet, but that’s okay. I opened this card to boost my credit and they gave me a chance when no one else would. My credit score jumped 100 points just with careful use of this card and on-time payments. I am thankful I opened this card, it has helped my credit a lot. I never had a problem with any of their reps so far. I make all my payments online for FREE. Yes it takes 8 days to post to the account, but if you read the terms booklet they send you with the card all of the fees are listed and they do tell you everything. I was aware of everything before I activated the card.

I applied for the surge card and got a statement before I got my card has that happen to anyone else

yes just got the statement but no card yet

These ppl charged me a late fee when their online site had not been processing my payment!!!!!!I told the uneducated rep that I have been on their site all week to make my payment and all it does is sit there and doesn’t go to another page to confirm my payment. The lady simply tells me that she can take my Paymnt for an extra $10.95 and will not credit my late fee. These ppl are greedy rip off scums!! I told her that they will not receive a Paymnt period and they can f**k themselves!!!!They will be talking to my bankruptcy attorney, so now who had the last laugh………….

Totally scam !! DO NOT USE THIS CARD. Once you active the card you are ruined!! Crazy statements !!! If you choose not to pay, their collection dep will be calling everybody in your family looking for you. very embarrassing ! DO NOT EVEN TOUCH IT !

I am a previous employee of Continental Finance, true the fees are excessive but if this is a second chance card for you, in order for you to build your credit you ABSOLUTELY MUST DO YOUR OWN RESEARCH, getting approved for a card is the easiest part of the deal. I have witnessed thousands of people get this card & max it out then complain to “us” that we have ruined their credit. First & foremost in order to build credit with a credit card it is strongly encouraged that you keep your utilization at 30% or less of your credit limit. This will go over some of your heads still. As a company they are in it to make money but if you do the research & don’t max the card out it can be beneficial to you, if you don’t agree with the $10.95 fee chose the online option to pay FREE, granted it counts for the DATE the payment is dated for however it takes 8 business days for that payment to become available but if your rebuilding, you shouldn’t be so anxious to spend the amount you just paid. The complaints are from the people who don’t really understand credit or “billing cycles”. ANYTIME you make a payment to a credit card you should be double checking on that payment to be sure it’s posted correctly. Their is still great hope for you. Take responsibility for YOUR OWN CREDIT. Stop expecting big name companies to hand walk you to the finish line. I have tead a lot of bad reviews but their are also people who have opened this card used it WISELY & are now home owners. EDUCATE YOURSELVES PEOPLE

Thank you for chiming in on this Anonymous. Can we wire funds to CF? I know exactly what I am getting into with this card and I have a 24 month plan. I can confirm that the CF rep told me CLI is given after 1 year of on time payments. I can’t confirm if this is true though, can you Anon? Also, I made my 1st payment on the website Aug 20th and the avail credit was made today 29th, so the 8 day hold is spot on. Is the 8 day hold firm? is there a quicker way such as wiring CF or faxing CF my internal bank ledger verifying the funds posted? BTW this is for the Surge card. What is the difference between the Surge Verve. Matrix and CF cards?

Yeah it will always take 8 days for the credit to become available. But as long as it clears your bank acct a customer service rep can do a conf call to your bank to confirm that the pymt cleared and they would be able to release the funds to you in 2 hours. For a payment to process faster you would have to use a debit card over the phone and it would be avail at midnight that night, but there is a 10.95 fee to make a payment over the phone.

i have a verve card and i cant never seem to be able to log in my payment is due today been trying for the last week to get the sight to come up buy i just get a error saying this sight is no good i refuse to pay the fee if it is something wrong with your website

how can i make a payment to my vervecard account

How can i make a payment on my verve card on line?

joe, you need to sign up for that at the verve website.

I have had this card for about 7 months now. I paid the 125 as soon as I activated the card. I have been paying when I have a balance with a debit card and it posts the next day but of course there is the 10 dollar payment charge they say is what WU charges them which is BS. All my bills are paid via WU speed pay and its like 3 dollars and shows as a separate charge. And no matter what your balance is even if its 20 dollars they always say 35 dollar payment is due bla bla. It does report well to the cb’s so if this is your only choice carry a zero balance for the first year then get another card and drop this card. I honestly don’t understand how they are allowed to operate like this.

OK so I miss placed my card. They were so rude to me not even trying to help. They asked me off the wall questions that didn’t make any sense to Me

I will pay off and cancel as soon as I can. I was just trying to build up my credit score it’s not worth it to me

I recently applied for and received a Verve card. After reading the reviews and discussions on it, something I should have done before I applied, I have decided not to activate it. They just want too much and too many fees. I appreciate the reviews and advice given out by consumers who have had bad experiences with verve. Pure and simple greed is all it is for a company to charge more knowing most consumers are trying to get their credit together and make the right choices. Well the right choice on this card is simple: Leave it alone.

I got the verve card in January..I was a little put off when I got a bill before the credit card. Then I called to activate the card and the rep told me that the best customers make a payment when they activate the card. After I told her four times I was aware of when my payment was due. I recently paid the card off to a zero balance and closed it!!!!!! Bye Felicia

Reading these statement can really make you think twice about how we balance what’s really important about our credit scores. At this point I’m just happy to get a second chance with a small price to pay. We are all just numbers,our credit score is worth more than our money these days. Just look at it as credit repair boot camp. We’ll win at the end. Stay strong and don’t abuse what we have now, before you know it the big hitters will be begging for our business….I feel everyone’s credit pain

The fees on this card are excessive, it’s a shame that Verve has such a strong marketing presence as I feel like a lot of people with bad credit think a card like this is their only option which couldn’t be further from the truth.

This card is a scam!!!! I’ve never heard of being charged an extra $10.95 to make a payment by phone…..

Michelle, If you pay with over the phone, call 1 Or 2 days before your due date and postdate your payment for your specific due date, no payment fee. Then wait till it clears your bank then call contenintal finance for a 3rd party conference call with your 1800- bank #, and request for an “emergency” funds release within 2hrs… Thats if you feel up to the matter, best way to get your funds for free and never be late…

They have the worst payment options ever. They only offer mail-in, bank account, or western union payments. It would be better if they would offer rapid reloads, walmart payments, or debit card payments. Most would compare this card to first premiere but it’s not even in the same league. The worst card ever.

I made a payment on 3/5…rec’d email confirmation of the payment. Payment hasn’t posted to my bank account yet-and no attempt was made. The payment is reversed on their website with no reason given…and different screens list different dates. Once screen says the reversal was right after the payment…another screen says reversal was yesterday? I’ve taken pictures of my bank account from the day before I made the payment until now-showing the funds have always been there and no attempt was made. Now I was billed $25 yesterday for a late payment? Really? I also haven’t rec’d any emails saying anything about the payment. So I’ll have to pay $10 by phone tomorrow…and they’re counting on the fact that I won’t have time to hassle over the $25. Guess this is how they’re going to pay their fine! Should be illegal…I have a payment confirmation number!

Possibility that you could of input an improper number or so when you were typing them online….Try calling your payment in 2 days before your due date and postdate it for your specific due date.no fee!

Everyone gets a confirmation number it just confirms that you SUBMITTED a payment but a confirmation number doesn’t mean your payment Has cleared your bank. A company won’t find that information out until they attempt to submit it to your bank. If their is an error in your routing or account number the payment will return.

I just recently received the Verve card but decided to not activate it. I have received two bills and have called twice asking how I can be billed on something that I am not even using. Both times they have told me it will be taken care of yet it is showing I am past due. I am concerned this is going to affect my credit and pretty sure this is illegal. What do I do if they dont stop billing me for a card that I didnt activate?

Same thing happened to me! I got a bill today, even though when I got the card I decided to not use and the auto message said I would not be charged or receive any fees since I denied the activation. Well today I get a bill in the mail saying I have a late fee and owe almost $200. Did you ever get this resolved? I’m thinking lawsuit.

they just sent me a bill i never even activated the card. and i got a bill for 125 dalliers!! did anyone solve this!!