Overview

![]() The First Premier credit card (also known as 1st Premier and Premier Bankcard) is a credit card marketed to applicants who have extremely bad credit. Unlike a secured card or a prepaid debit card, the First Premier card functions as a traditional credit card, allowing users to spend money up to a set credit limit and then pay their balance off at the end of each month. First Premier advertises that the card “may be able to help build, rebuild, or reestablish credit history if on-time payments are made to all of your creditors and account balances are kept low relative to the credit limit.”

The First Premier credit card (also known as 1st Premier and Premier Bankcard) is a credit card marketed to applicants who have extremely bad credit. Unlike a secured card or a prepaid debit card, the First Premier card functions as a traditional credit card, allowing users to spend money up to a set credit limit and then pay their balance off at the end of each month. First Premier advertises that the card “may be able to help build, rebuild, or reestablish credit history if on-time payments are made to all of your creditors and account balances are kept low relative to the credit limit.”

First Premier formerly offered two different credit cards (the Aventium card and the Centennial card), but it appears to only issue one MasterCard credit card at this time. This card comes with a $300 credit limit (subject to variation based on creditworthiness) and does not offer any kind of rewards or cash back program.

First Premier Fee Breakdown

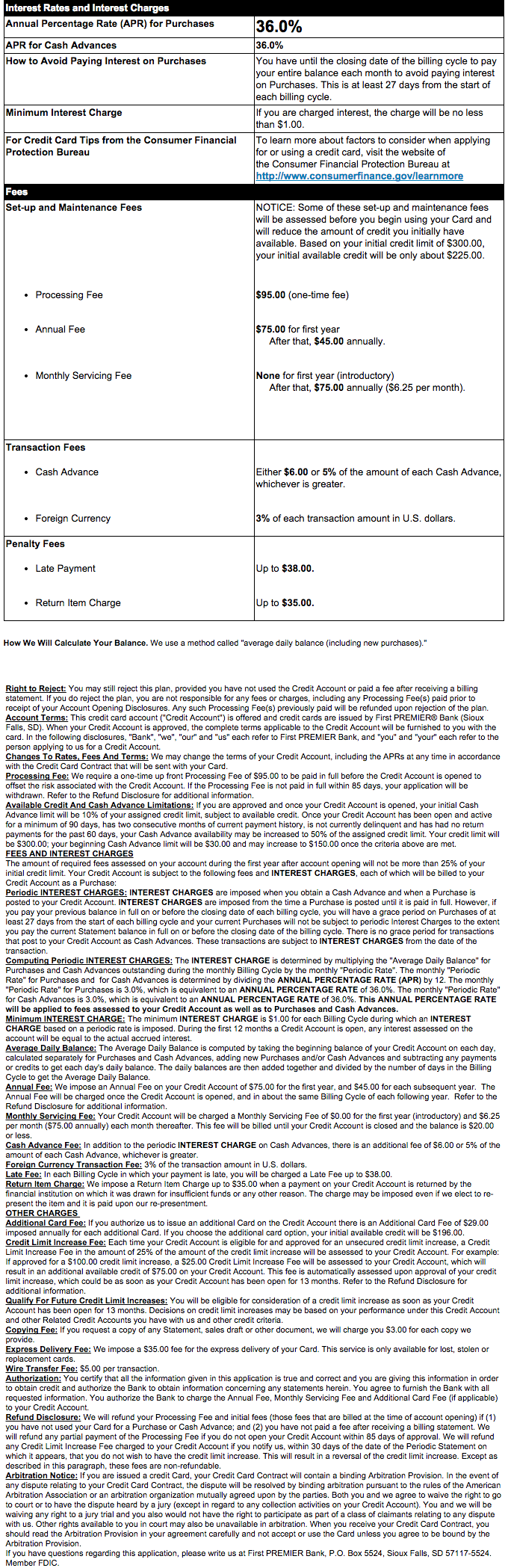

The First Premier credit card charges a one-time $95.00 processing fee before approval, a $75 annual fee for the first year (which drops to $45 in the second year), an interest rate of 36%, a monthly fee of $6.25 starting in the second year, a fee of either $6 or 5% per cash advance (whichever is greater), a 3% per-transaction fee for foreign currency, a late payment fee of up to $38 per incident, a return item fee of up to $35 per incident, $3 statement fee, and a fee of 25% of the credit limit increase each time the company unilaterally increases the cardholder’s credit limit. There may also be other fees depending on conditions not listed below. All of these fees are charged to a card that initially has a limit of $300.

First Premier Credit Card Fees

At a glance

Founded: 1929

Location: Sioux Falls, South Dakota

Issuer: First Premier Bank

Website: Numerous, including firstpremierbankcardgrey.net, premiercreditcardsf.net, and premiergoldcards.net

Phone number: 800-987-5521

E-mail: n/a

What other reviewers are saying

Ripoff Report

![]() There are over 550 negative First Premier reviews on Ripoff Report dating back to 2002, and it appears that these complaints have been filed regularly over that period of time. Complainants primarily cite excessive fees, nondisclosure of terms, poor customer service, billing errors, deceptive sales tactics, and aggressive collections practices. In many cases, it appears that the reviewers had a firm understanding of fees charged by First Premier in the first year of service, but did not anticipate the increase in fees that comes in the second year. The company does not appear to have responded to any complaints.

There are over 550 negative First Premier reviews on Ripoff Report dating back to 2002, and it appears that these complaints have been filed regularly over that period of time. Complainants primarily cite excessive fees, nondisclosure of terms, poor customer service, billing errors, deceptive sales tactics, and aggressive collections practices. In many cases, it appears that the reviewers had a firm understanding of fees charged by First Premier in the first year of service, but did not anticipate the increase in fees that comes in the second year. The company does not appear to have responded to any complaints.

The Better Business Bureau

![]() The BBB currently awards Premier Bankcard an “A” rating and accreditation despite 1,001 complaints filed against the company in the last three years. The bulk of the complaints (716) are related to billing and collection, with product and service issues coming in a distant second (238). The company has resolved just over 80% of the complaints to the customer’s satisfaction, while the remaining disputes were resolved to the dissatisfaction of the customer. The BBB has kept a profile for Premier Bankcard since March 2003.

The BBB currently awards Premier Bankcard an “A” rating and accreditation despite 1,001 complaints filed against the company in the last three years. The bulk of the complaints (716) are related to billing and collection, with product and service issues coming in a distant second (238). The company has resolved just over 80% of the complaints to the customer’s satisfaction, while the remaining disputes were resolved to the dissatisfaction of the customer. The BBB has kept a profile for Premier Bankcard since March 2003.

Other sources

First Premier currently has a 1.4 out of 5 rating on Consumer Affairs, a 1.7 out of 5 rating on Credit Karma, and a 3 out of 5 rating on CardHub. CreditCardForum.com gave the card a negative review, calling it “nothing but a classic horror story.” NerdWallet also wrote a scathing review of First Premier titled “Please Don’t Get a First Premier Credit Card.”

Featured User Reviews

This company doesn’t just charge high fees they are total crooks. Thieves who found a loophole in the system that allows them to legally steal money from good people trying to lives back on track.

Case in point:

Lost my business which resulted in my credit being tarnished beyond bad. Trying to rebuild my credit I applied for and got a FP credit card. I always paid my outstanding balance in full and ahead of time. Without warning FP blocked my account and disallowed me from using it even though I had no outstanding balances or late fees. When I contacted them, a rep said they blocked my account because I made ‘excessive payments’ and until I proved to them in writing I actually made these payments my account remained blocked.I refused to do that because I couldn’t believe what I was hearing: being blocked for making numerous payments early? I had to be dreaming. I wasn’t, in fact my nightmare with First Progress was just beginning.

2 months after this fiasco I get a letter from FP saying I owe them a $39 annual fee. A month later I get yet another letter from them saying I now owe them $39 fee plus $37 late fee.

Not wanting to mess up my credit even further I paid FP the money they stole from me and told them to close my account permanently.

I know when your credit is just awful and you have to depend on sharks to get you back on track it can be a bit scary. I suggest you open a secured credit card instead. But if you can’t, whatever you do, DO NOT get a credit card with First Premier. They are thieves. This is an unethical company. YOU HAVE BEEN WARNED!!!!

-Lode Loyens, NerdWallet

The First Premier Bank of Sioux Falls SD specializes in damaging one’s credit scores while gouging them with obscene fees and rates for credit cards.

For starters, these greedy banksters primarily target low income individuals (especially single women living in section 8 projects) with little or no established credit histories. They dangle a $700 Master Card credit line “deal” card that comes with an initial $175 annual fee for the first year, coupled with a whopping 36 percent APR (annual percentage rate). After the first year is up, they get a $49 annual fee plus a $14.50 per month “Monthly Service Fee (which is actually $174 addition charges annually)” for allowing the card holder recipient to effectively kiss the bank’s ring.

There are also many other insulting stipulations, such as: “Each time your credit account is eligible for and approved for an unsecured credit increase, a Credit Limit Increase Fee in the amount of 25 percent of the amount of the credit limit increase will be assessed to your Credit Account. For example: If approved for a $100 credit increase, a $25 Credit Limit Increase Fee will be assessed to your credit account. This fee is automatically assessed upon approval of your credit limit increase, which could be as soon as your credit account has been open for 13 months.”

To add insult to injury, a new account holder will have already reached 25 percent of their available credit utilization ratio, which will go above 30 percent with the first purchase over $35. As such, the card holder’s FICO and Vantage scores, respectively, will be lowered on top of the points lost for the initial Hard Inquiry to their personal credit report.

In sum: First Premier Bank is a shameless blood sucker and should be boycotted by anyone who understands shady or unethical business practices that often do far more harm than good, and generally speaking, make certain that the Have Not’s will continue to have even less.

-Jacheart, Ripoff Report

Our take

First Premier is a bottom-tier option for all cardholders regardless of credit score. It charges very high fees and interest rates and offers a very low credit limit with no rewards or cash back. The company explains its pricing by claiming that it needs to charge higher fees to offset the losses associated with its poor-credit user base, but this explanation does not make its pricing any more appealing. To make matters worse, many customers also report poor customer service, aggressive collection tactics, and occasional billing errors. All things considered, this card seems more likely to drive drive users further into debt than to repair their credit scores.

If your credit score is extremely low, you can still build credit without resorting to a card as expensive and demanding as the First Premier Credit Card. Secured credit cards can help you rebuild your score and limit your exposure to harsh penalties and high interest rates. If you need a simple payment card, then you can qualify for a checking account or even a prepaid debit card with minimal hassle. According to nearly every third-party resource we found, almost any option is better than First Premier.

Have you used a First Premier credit card? Tell us about your experience in the comment section below:

OK so heres my sad tale I am a senior citizen on a fixed income When I applied for this card I had a $600 a month income and my ex husband had literally abandoned me I was living in a housing authority building on welfare food stamps didnt even have a car my credit score was BELOW 500 due to ex husband and well being BEYOND poor Ok so I knew what I was getting into but heres the thing They gave me a $300 limit then charged the card almost a hundred dollars to “activate” the interest was HORRIBLE but I literally used this card TO SURVIVE to EAT and buy things my food stamps wouldnt So ok heres the really horrible part NO ONE told me that was a yearly fee so the next year the card was MAXED and they charged their fee then proceeded to charge INTEREST on that and over the limit fees so I tried to talk to them and of course thats impossible so I requested an increase in the limit which they would NOT do but said I could get another card so I did that and now I got TWO cards for the same limit and yet they would NOT raise the credit limit and I was a customer with the first card for quite some time made the payments and even paid the bogus fees but then dont even let “life happen” like it does I moved and I had all the expenses that go with that so I called them and told them I cant make the payment this month could you defer it NO please dont charge me over the limit and late fees I am telling you UPFRONT before it happens my situation NO please could you combine these accounts so I have ONE payment and ONE set of fees instead of TW? Even so I tried to keep up tried to keep it paid I was really trying to just SURVIVE here I wasnt even buying anything of value I wasnt going on trips or nothing it literally was stuff like FOOD toilet paper PET food essentials Then I got a raise in income so I tell them I just want to pay this off but before I do I want you to STOP adding fees and then charging INTEREST on the fees they refused so I stopped paying It went on and on and on just climbing and climbing til it was literally DOUBLE the original credit limit which PS THEY REFUSED TO RAISE so then I call them after they send me a so called “settlement offer” before charge off and they say they will NOW STOP charging all the fees and interest on top of that if I will agree to AUTO PAYMENTS and make those payments without stopping so I agreed First payment comes due and I notice they did NOT keep their end of the bargain and there were addtional fees I called them I tried to stop the auto payments with them and the bank because first of all they broke their word so I wasnt about to let them take what was essentially almost my entire income for PAYMENTS so I go to my bank they would stop it either so I withdrew the funds to SURVIVE you know pay rent and EAT and the bank proceeded to charge me over $300 in fees and so now instead of bad credit from a bad marriage and on and on I now have still after TWO YEARS this debt continually reported to the credit bureaus THREE TIMES and the disputes do no good cause they keep coming back as VALID debts and insult to injury go to the BBB which as is stated here they are BORDERLINE LEGAL on that entity and I cant even stress enough this is not the only card that does this there is Credit One One other entity called Bank of Missouri with various names There is one under the umbrella of Celtic and I had all those as well ALL LOW balance HIGH interest that are worse than loan sharks who used to break your legs These people break your bank account your already BAD credit gets worse They will break your hopes to ever improve your situation and they will break your heart and even your will to live I also have used those rip off payday loan places that charge 300% interest just to have a tooth pulled that went on for TWO years These people are all blood suckers FINGERHUT COMENITY BANK SYNCHRONY and PREMIER and all these bottom feeders who prey on the OLD the SICK the POOR the ones who cant already cut a break in this life and then add insult to injury some of them sell them to third party debt collectors and those bottom feeders second down the chain add to them the attorneys who work for them and they would be even further down the food chain…I will say I had a measure of success ….I got the lawsuit dropped and DISMISSED cause here they are suing me in the middle of a pandemic when CRIMINALS arent even required to go to court and even so I cant get those bloodsuckers the third party entities to stop report this to the credit bureaus Premier is smart they dont take that chance they KEEP that debt like its written in STONE but its not its written in BLOOD and the blood is the lifesource of the people they PREY ON I dont think its going to do any good to complain anymore I am just going to have to wait them out I even thought about trying to settle again but I am LITERALLY afraid to try They are EVIL and need to go down with the rest of this rotten system we are all greasing the wheels of with our souls If you are considering this as ANY Kind of alternative to help you in your life or aid you in your desire to do better and maybe have SOMETHING in this life before you die DO WITHOUT you will be much better off I would have been better off to STARVE that was temporary while this evil entity just lives and breaths and never goes away

Horrible credit card. Very high interest and high annual fee. I called to close my acct and found out they leave it open. The company took my auto payment even when i do not have a balance.

I’m in the hospital I will pay u next month I’m sorry I couldn’t get it done this definitely I will in April ok James card

First premier bank

is a bad company , avoid using them even if you want to rebuild your credit . They are only here to steal your money bad bad bad company I can testify that I have been a victim of first premier scam .

This company has to face a class action lawsuit even going to small claim is advisable . I notices a fraudulent act on this company. I will also advice not to open account with this company due to their numerous manipulation act to steal from you and then closing your account for no reason after collecting so much from you . Am preparing to sue if they dent my credit . People should collect evidence . This company told me to that there was an issue with my account but will not tell me until I pay them $80 before they will tell me what is wrong

First Premier has the most prehistoric online system. No statements available, no year end info available. Can only go back a few months, and they want to charge fees to provide what they should be providing online! The most user unfriendly credit card I’ve ever had.

They are crooks they stole my money

I have a credit card with them and this is one of the worst companies I never had to deal with. The company do not appropriate thier customers they charge you 25 percent to do a credit increase. I would not recommend this company nor this card to no one especially if you are trying to build your credit…THEY ARE FULL OF SHIT…. NEVER AGAIN !!!!!! AND I WILL BE CALLING THEM TO THE BETTER BUSINESS BUREAU… THIS COMPANY IS A RIP OFF….

STOP do not acceptor request any cc from this bank. total ripoff. I called customer svcs about charges and attempt to update my bill. the rep took my payment twice continuing to state it was only registered once which I referred to a supervisor, two weeks later I received a letter fro them for a refund but they continue to charge me late fees now they are trying to bill me 207.00 from a month ago with fees of $57 with an amount overlimit of $121.00 interest of $17. after talking to a customer svc agent she was rude and stated there was nothing to be done but pay

Beware of this bank. I don’t have an account with them but they saw fit to take $95.00 out of my Bank of America account for a fee for a card that I don’t have. Can’t talk to anyone because their phone system sucks. I found another number to call so will try Monday. 800-501-6535 I wonder if I can talk to someone at that number. I guess they give credit and debit cards out with asking for ID. I feel that this a rip off and they should be prosecuted for the way the do business.

I never received the credit card that I was approved for. So I was wondering did you guys send it to the correct address…..